In 2025, rising inflation, job instability, and unforeseen emergencies have pushed many Indian borrowers into loan defaults. If you’re facing difficulties repaying your personal loan, credit card bill, or business loan, you may have heard terms like “loan write-off” and “loan settlement.”

Though both involve unresolved loans, they are very different in meaning, impact, and consequences. Misunderstanding the difference can lead to confusion, especially when dealing with banks, NBFCs, or even legal notices.

In this guide, we’ll break down loan write-off vs. loan settlement, their effects on your CIBIL score, legal implications, and how Guardian Financial Experts can help you make the right choice.

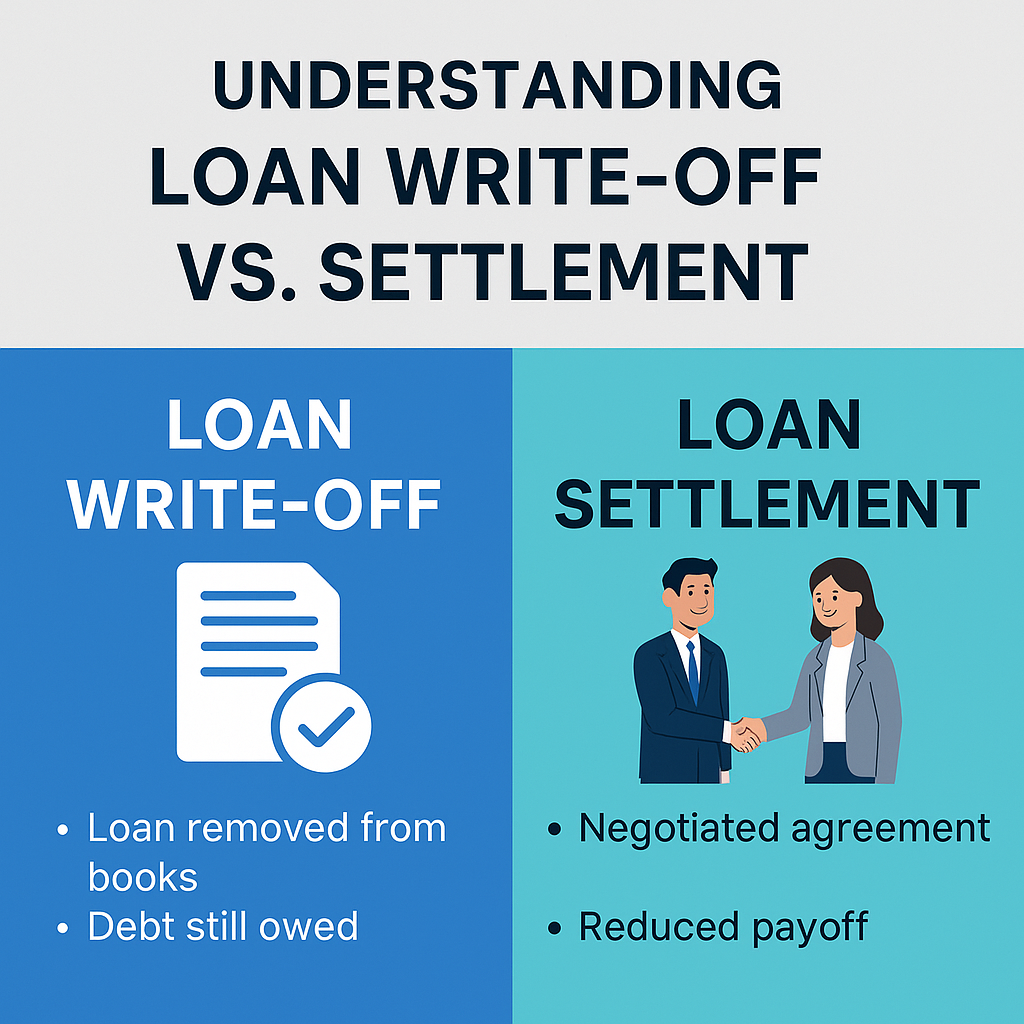

📘 What Is a Loan Write-Off?

A loan write-off is an accounting process used by banks or NBFCs when they believe that a loan is not likely to be recovered in the near future. This usually happens after 180+ days of non-payment (NPA status).

👉 In Simple Terms:

The bank removes the unpaid loan from its active books but does NOT cancel your loan obligation. The debt still exists legally, and the bank can take action later.

✅ Key Points:

- Used primarily for accounting and tax purposes

- Done when a loan becomes an NPA (Non-Performing Asset)

- Your loan isn’t forgiven—you still owe the money

- Appears as “written-off” in your credit report

- The bank may still recover the loan via legal means or recovery agents

📘 What Is a Loan Settlement?

A loan settlement is a negotiated agreement between the borrower and the lender to pay a lesser amount than what is originally due, as a full and final payment.

This typically happens when the borrower is:

- Facing genuine financial hardship

- Unable to repay the full amount

- Willing to pay a lumpsum or partial amount to close the account

✅ Key Points:

- Requires mutual consent between borrower and bank

- Usually involves paying 25%–70% of the outstanding balance

- After settlement, the bank closes the loan account

- The borrower receives a “Settlement Letter”

- Credit report reflects it as “settled” (not “closed”)

👉 Want to know more?

🔗 How People in India Are Settling Their Loans in 2025

🆚 Loan Write-Off vs. Settlement: Key Differences

| Aspect | Loan Write-Off | Loan Settlement |

|---|---|---|

| Definition | Loan removed from active books, but still payable | Negotiated reduced payment to close the loan legally |

| Initiated By | Lender (Bank/NBFC) | Borrower or jointly by both parties |

| Legal Obligation | Still exists | Cleared upon payment of settled amount |

| Effect on CIBIL | Shows as “Written-Off” – very negative | Shows as “Settled” – moderately negative |

| Loan Closure | Not officially closed | Closed with a settlement certificate |

| Recovery Possibility | Yes, lender may pursue legally or through recovery agents | No further recovery after settlement |

🔍 When Do Banks Write Off a Loan?

Banks in India typically write off loans when:

- The borrower has not paid for more than 180 days

- The loan is classified as NPA

- Recovery efforts have failed so far

- The bank wants to clean up its balance sheet

This is not forgiveness—it is temporary financial accounting. Banks still pursue recovery later.

Your CIBIL report will mention “Written-Off” or “Written-Off (Settled)”, which badly affects your creditworthiness.

🔍 When Should You Consider a Loan Settlement?

Loan settlement is a practical solution when:

- You’re unemployed or have no stable income

- You’re overwhelmed by debt or EMI bounce penalties

- You’re receiving legal notices or recovery agent calls

- You wish to legally close the loan with a reduced burden

💡 Guardian Financial Experts can help you negotiate 40%–70% reductions depending on the case.

🔗 What to Expect During Loan Settlement Negotiation

⚠️ Impact on Credit Score: Write-Off vs. Settlement

Many borrowers think both actions clean their credit—this is a myth. Here’s what really happens:

🟥 Loan Write-Off:

- CIBIL score drops by 100–150 points or more

- Remains on report for up to 7 years

- Makes you ineligible for future loans or credit cards

🟨 Loan Settlement:

- Credit score drops but is still better than write-off

- Shows as “settled” instead of default or written-off

- Possible to rebuild score faster after settlement

👉 After settlement, we at Guardian Financial Experts also offer a Credit Repair Program to help restore your CIBIL score quickly.

🛡️ Legal Consequences of a Written-Off Loan

A write-off does not prevent legal action. Even if your loan is written off:

- The lender can still file a civil recovery suit

- You can be summoned to court

- You may receive notices under the SARFAESI Act

- You may be harassed by third-party recovery agents

🛑 If you’re facing this, don’t wait—contact Guardian Financial Experts immediately to settle legally and avoid escalation.

✍️ How to Know If Your Loan Was Written-Off or Settled

You can check your CIBIL report to confirm. Visit:

🔗 https://www.cibil.com

In your report, look for:

- Account Status: Will say Written-Off or Settled

- Write-Off Date

- Outstanding Balance

- Written-Off Amount

If you see “written-off” and haven’t settled it, banks can still pursue legal action or sell your debt to third-party agencies.

🧾 Which Is Better: Loan Write-Off or Settlement?

✅ Loan Settlement is Always Better, because:

- You legally close the loan

- You get a No Dues Certificate

- Recovery agents will stop contacting you

- You can rebuild your credit faster

- You have a record of trying to resolve your debt

In contrast, write-offs give you no control, invite legal trouble, and damage your credit further.

🤝 How Guardian Financial Experts Can Help You

If your loan has been written off or is on the verge of default, don’t panic. Let our legal-financial team help you negotiate directly with the lender and:

- Stop harassment by recovery agents

- Avoid court proceedings

- Get up to 70% reduction on dues

- Receive legal closure letters

- Rebuild your CIBIL score with our support

We specialize in:

🔹 Personal Loan Settlements

🔹 Credit Card Dues

🔹 NBFC & Fintech Loan Closures

🔹 Legal Notices & Recovery Protection

🎯 Contact Guardian Financial Experts for a free consultation today.

📝 FAQs on Loan Write-Off vs. Settlement

Q. Can I get a loan after a write-off?

Not easily. Your CIBIL will show a bad history, and most lenders reject applications.

Q. Can I settle a written-off loan?

Yes! In fact, settling it later helps reduce legal risks and shows responsibility.

Q. Will banks agree to a 30–50% settlement?

Yes, especially if your account is NPA or written off. Guardian negotiates such cases daily.

Q. Can recovery agents harass me after a write-off?

They’re not supposed to, but many do. You have legal rights to stop them.

Q. Is settlement better than write-off?

Absolutely. It’s always better to settle than to be labeled a defaulter.

📌 Conclusion: Don’t Wait—Take Action Now

In India, more borrowers are opting for loan settlements in 2025 than ever before. If your loan is heading towards write-off or if you’ve already received a legal notice—act now.

Choose a legal, ethical path with Guardian Financial Experts and resolve your debt smartly.

🛑 Don’t wait for your loan to be written off.

💬 Settle. Close. Rebuild.

💡 Need Help?

📞 Call us or visit 👉 www.guardianfinancialexperts.com

📩 DM us your case for a free consultation

🧾 100% Confidential | ✅ Legal Process | 🛡️ RBI-Compliant