Dealing with overwhelming debt is never easy, especially when calls from banks and recovery agents become a daily reality. Many borrowers, while trying to manage things on their own, make avoidable mistakes that worsen their financial situation. Loan settlement may sound like a simple negotiation, but it’s a complex process that involves strategy, documentation, legal awareness, and understanding of how lenders actually operate. Without expert guidance, borrowers often fall into traps that cost them time, money, and peace of mind.

Below are the most common mistakes borrowers make when handling loan settlements without professional support — and why having an expert by your side can make all the difference.

1. Ignoring Communication from Banks

One of the first and most damaging mistakes borrowers make is ignoring calls or notices from lenders. Out of fear or frustration, many stop responding once they’ve defaulted on their EMIs. Unfortunately, silence never helps. When you stop communicating, banks interpret it as unwillingness to cooperate, which can accelerate recovery actions such as initiating legal notices or marking your loan account as a written-off asset.

A loan settlement expert understands how to maintain controlled and strategic communication with lenders. They ensure that every interaction works toward your benefit — protecting you from harassment while keeping negotiation channels open.

2. Attempting to Negotiate Without Knowledge of Bank Policies

Every bank has distinct policies and internal criteria for approving settlements. The percentage of waiver, approach to different loan types (secured vs. unsecured), and timing of offers vary from lender to lender. Borrowers who approach negotiation blindly often get rejected or accept unfair terms.

Professionals in debt resolution have in-depth experience with multiple banks. They know when the bank is most likely to consider a settlement proposal and what documentation or hardship proof can strengthen your case. This insight often proves the difference between getting a 30% waiver and achieving a 60% or higher settlement.

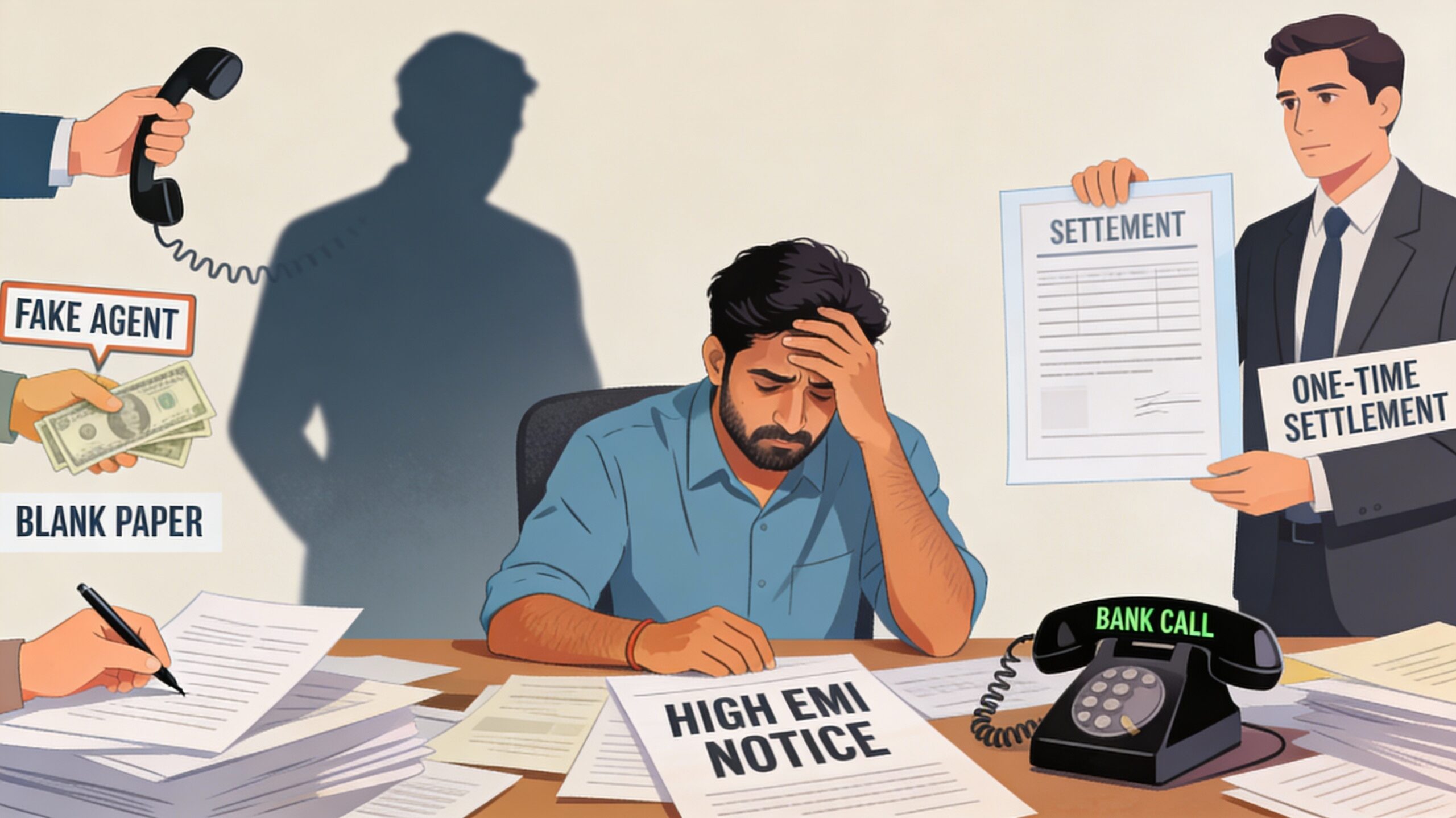

3. Falling Into Debt Collection Traps

Debt collection agencies are trained to push borrowers emotionally, often using psychological tactics to pressure payments. They may promise unrealistic settlement offers over the phone just to collect part-payments and then deny any written confirmation later. Borrowers acting alone often fall for such verbal promises or hand over signed blank papers, making things even worse.

A settlement expert acts as a shield between you and the recovery agents. Everything is documented properly, negotiations are legally compliant, and promises are verified before you make any payment. This transparency prevents exploitation and ensures your rights as a borrower are protected.

4. Misunderstanding the Credit Score Impact

Many borrowers believe that settling a loan “clears their record.” In reality, a settlement is reported as “Settled” or “Partially Paid” in the credit bureau records — which affects creditworthiness for several years. Without proper planning, this can make it difficult to secure new loans or credit cards in the future.

An experienced settlement advisor not only focuses on reducing your debt burden but also helps you rebuild your credit profile after the process. They guide you on steps such as obtaining a No Dues Certificate, verifying closure updates in your CIBIL report, and gradually improving your score through responsible repayment habits.

5. Paying Unverified Agents or Fraudulent Consultants

In desperation, some borrowers turn to unverified third-party agents promising “instant loan settlement.” These individuals often charge upfront fees and disappear, or make illegal offers on behalf of the borrower that damage the negotiation process. Many victims end up losing money twice — to the agent and to the overdue interest that continues to grow.

Licensed or registered settlement experts operate through legitimate channels, maintain transparent fee structures, and ensure that banks officially acknowledge every step of the process. Before hiring anyone, always verify their credentials, online presence, client reviews, and success rate.

6. Missing the Right Timing for Settlement

Timing is everything in a loan settlement. Banks are more receptive to settlement discussions at certain stages — for example, after an account becomes NPA (Non-Performing Asset) or during quarterly closing periods when they review recovery targets. Borrowers who try to settle too early or too late often face rejection or less favorable terms.

A professional with experience in loan negotiation understands this timing. They can identify the stage when settlement becomes feasible and prepare your documentation to align with the bank’s internal process, ensuring maximum benefit.

7. Failing to Get Written Confirmation

Even when a borrower manages to negotiate an informal settlement, they often fail to obtain a written agreement clearly stating the outstanding amount, waiver percentage, and no further liability clause. Without such documents, the bank can later deny the agreement or sell the remaining dues to a collection agency.

Experts ensure every settlement is formalized through an official One-Time Settlement (OTS) letter from the bank. They verify that payments are made only to authorized accounts and update your loan closure correctly in CIBIL — ensuring there are no surprises later.

8. Emotional Decision-Making Instead of Strategic Negotiation

Debt can be overwhelming, and borrowers often make emotional decisions — either agreeing to whatever the lender says or avoiding the issue altogether. Such reactions usually worsen financial stress. A settlement expert brings objectivity and experience, analyzing each case logically to design the right strategy for negotiation, documentation, and repayment capacity.

By keeping the process professional, you reclaim control over your financial recovery journey instead of letting fear dictate your choices.

Final Thoughts

Loan settlement is not just about bargaining for a lower amount — it’s about managing risk, reputation, and long-term financial stability. Without professional guidance, borrowers often make costly errors that delay or destroy their chances of achieving true debt freedom.

With a trusted loan settlement expert by your side, you gain structured negotiation, legal protection, transparent communication with banks, and a realistic roadmap to becoming debt-free. The right help can turn a stressful situation into a manageable process — leading to lasting financial peace.