A loan settlement expert plays a crucial role in helping overburdened borrowers resolve high‑interest credit card dues and personal loan EMIs when regular repayment has become practically impossible. Even without access to live financial tools right now, the general principles of how these professionals work are well established and can be explained clearly.

Why Credit Card and Personal Loan Debt Is So Risky

Credit cards and unsecured personal loans carry high interest and penalties, so once you start missing payments, the outstanding amount can grow rapidly. Interest, late-payment fees, over-limit charges, and GST can all pile up on top of your principal. As a result, many borrowers find that even after paying for months, their total dues hardly reduce, which is where professional settlement support becomes useful.

- Credit card APRs are typically much higher than most other retail loans, so revolving balances quickly become a debt trap if only minimum amounts are paid.

- Personal loans are usually fixed‑tenure with fixed EMIs, so repeated defaults can trigger collection pressure and, eventually, legal escalation from lenders.

What Exactly Does a Loan Settlement Expert Do?

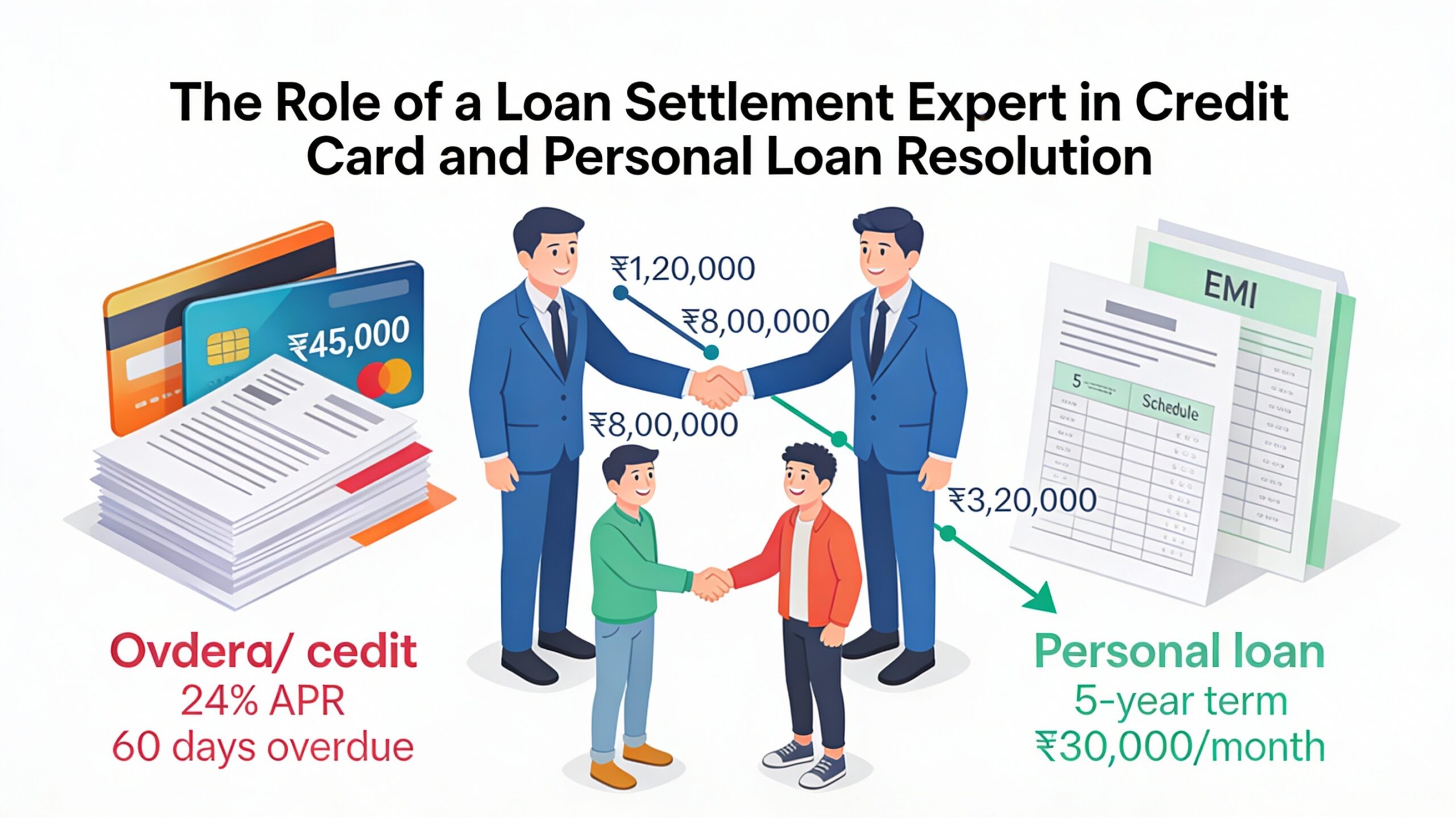

A loan settlement expert is a specialist (often a lawyer-led team, consultant, or debt‑relief firm) who represents you in discussions with banks, NBFCs, and card issuers to reduce and close unsecured debts. Their primary task is not to “magic away” your dues, but to convert an unmanageable situation into a realistic, negotiated resolution that the lender will formally accept.

- They conduct a detailed assessment of your income, expenses, assets, and all outstanding loans and cards to understand how much you can reasonably pay.

- They prepare a settlement or restructuring strategy: for example, a lump‑sum settlement, staged payments of a reduced amount, or combining multiple debts into a coherent plan.

- They open a formal line of communication with lenders, sending letters and emails, and negotiating terms on your behalf while you step away from daily confrontation.

Role in Credit Card Resolution

With credit cards, the expert’s focus is on tackling very high interest and accumulated penalties that make the dues balloon. Since a portion of the outstanding amount often consists of fees and compounding interest rather than pure principal, there is usually some room for negotiation.

- They work to secure waivers or reductions of late fees, over-limit charges, and part of the accumulated interest so that you pay closer to the principal plus a reasonable margin.

- In many cases, they negotiate a “full and final” settlement, where you pay an agreed lump sum (often in one or a few instalments) and the bank closes the card account.

- They ensure that, after settlement, the card is blocked for future use, statements show zero operational balance, and you receive a written confirmation so the same debt is not chased again.

Role in Personal Loan Resolution

Personal loans are structured differently from cards, but once EMIs are missed for several months, lenders may be willing to discuss settlement or restructuring rather than pursue long, costly recovery processes. Here, the expert positions your financial hardship in a way the lender’s risk and legal teams can accept.

- They may ask the lender to restructure the loan: extending tenure, reducing EMI, or temporarily lowering interest so that you can resume payment rather than default completely.

- Where your finances are severely affected (job loss, business failure, medical emergency), they negotiate for a reduced “one‑time settlement” amount to close the loan.

- They carefully review the settlement letter to ensure it clearly mentions “full and final settlement” and specifies amount, date, mode of payment, and that no further dues or interest will be claimed.

Protecting You from Harassment and Legal Confusion

Beyond pure numbers, one of the biggest contributions of a loan settlement expert is shielding you from the emotional and psychological pressure that often comes with overdue credit card and personal loan accounts.

- Once formally authorised, they ask lenders to route communication through them, which reduces direct calls, threats, or confusing conversations with recovery agents.

- They help you distinguish between genuine legal notices and mere pressure tactics, explaining what actions a lender can realistically take and what is unlikely.

- If lender behaviour crosses ethical or regulatory lines, they can guide you on how to respond in writing and, where appropriate, how to lodge formal complaints.

Managing the Impact on Your Credit Score

Both credit card and personal loan settlements affect your credit report, but an expert helps you use settlement as a damage‑control tool rather than an uncontrolled collapse. The goal is to accept some short‑term score impact in exchange for long‑term stability.

- They explain how different outcomes are reported (for example, “settled” versus “closed”) and what that means for future loan and card eligibility.

- They push lenders to update bureau records correctly after you honour the settlement, reducing the risk of lingering negative remarks beyond what is unavoidable.

- They then guide you on rebuilding: small, well‑managed credit, on‑time payments, and disciplined use of any new facilities over the next few years.

When Should You Consider Using One?

A loan settlement expert becomes particularly valuable when you are simultaneously facing multiple card dues and personal loan EMIs, and your income can no longer support all of them even with strict budgeting. If calls are frequent, legal terms in letters feel overwhelming, and you are unsure whether to keep paying minimums, stop paying, or ask for a specific solution, that is a strong indicator that professional guidance can prevent costly mistakes.

In short, the role of a loan settlement expert in credit card and personal loan resolution is to stand between you and a spiralling debt situation—turning scattered overdue bills, high interest, and emotional pressure into a structured, negotiated plan you can actually complete, while ensuring the closure is documented properly so you can start rebuilding with confidence.